Commentary

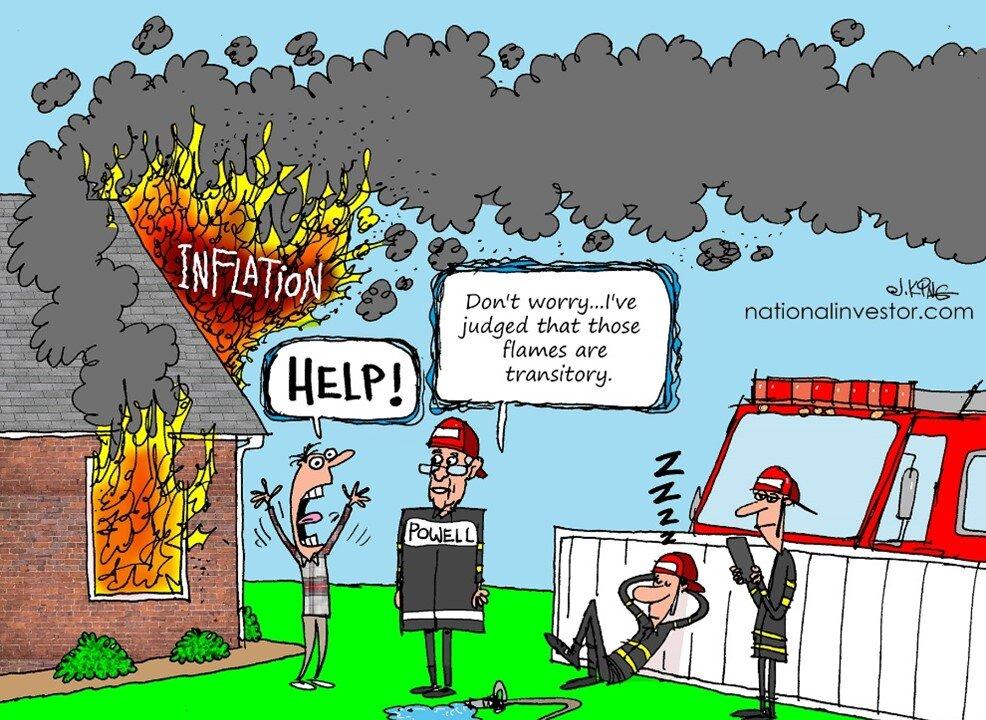

As I write this, the Bank of England has just raised its benchmark short-term rate for the second time in the recent past. The European Central Bank stood pat at its Feb. 3 meeting; but beset by inflation at a multi-decade high, it is inevitable that the ECB will get dragged into the nascent inflation-fighting across the globe sooner rather than later.