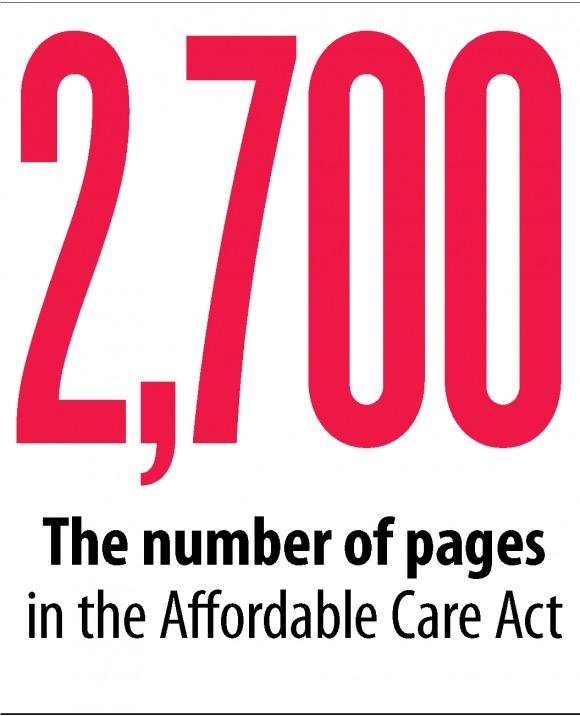

President Donald Trump and the Republicans have no choice about replacing the Patient Protection and Affordable Care Act (ACA), as the law is generally recognized to be failing. But how to replace this giant law that has affected every part of American society is a matter of urgent and ongoing debate.

*