(L-R) Harvard Law Professor Elizabeth Warren talks with White House Economic Recovery Advisory Board Chairman Paul Volker and Commerce Secretary Gary Locke before the signing ceremony for the financial reform bill at the Ronald Reagan Building and International Trade Center in Washington, D.C., on July 21, 2010. Chip Somodevilla/Getty Images

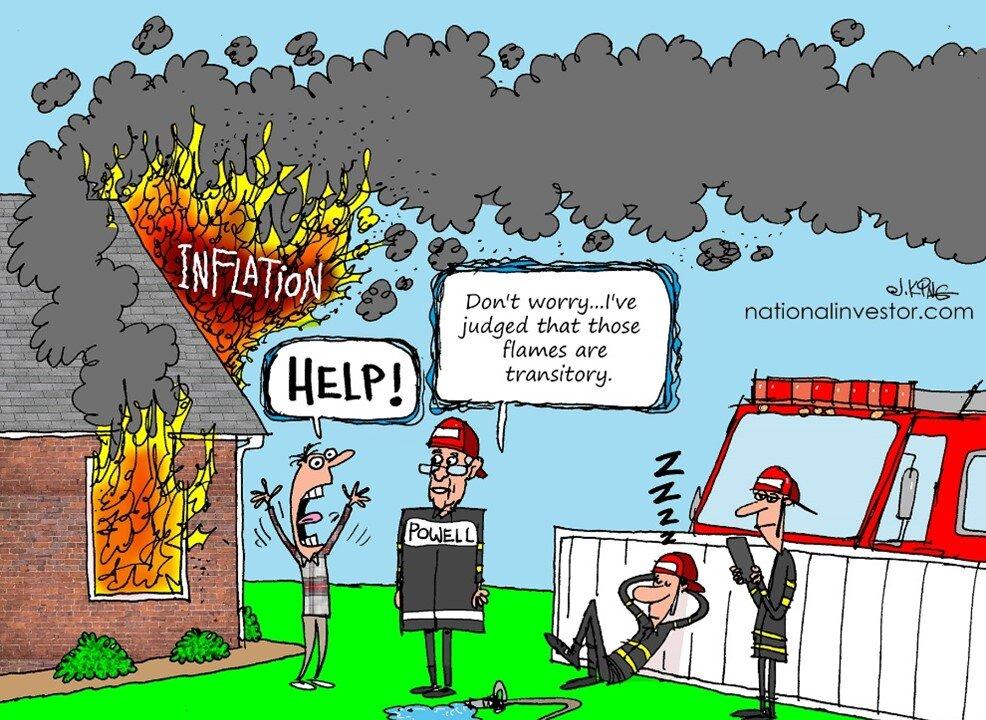

It’s become fashionable recently to invoke the memory of the late Paul Volcker, with consumer prices rising at their fastest rate since he ostensibly vanquished the double-digit price inflation of his watch. Saddled himself with the political mess he inherited from a tanking U.S. dollar and soaring prices, former President Jimmy Carter finally appointed Volcker as Fed Chairman in the summer of 1979 to do something about all this.

Chris Temple

Author

Chris Temple has set himself apart with his unique ability to make the intricacies of the markets and our world understandable to the average person, chiefly via his newsletter The National Investor. With over five decades in the financial and investment world, his commentary has appeared in Barron’s, Forbes, Investors’ Digest, among other publications. To discover how to get his proprietary research in the paid newsletter service, go to The National Investor.