If the Chinese yuan devalues against the U.S. dollar, “officially” or otherwise, it could dramatically alter the economic status quo of the past two-plus decades and it will be for the worse.

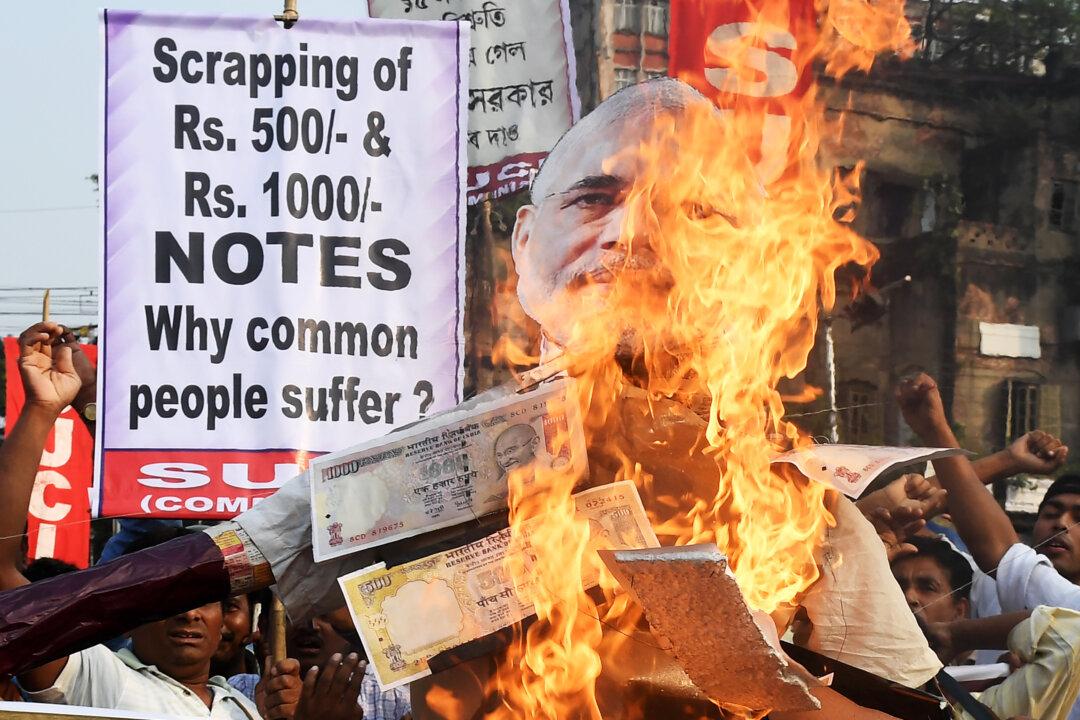

The Mainstream Media, labels the ongoing plunge of a plethora of non-Western currencies an “Emerging Market” crisis. However, such “emerging markets” include some of the world’s largest – particularly, the “BRICS” nations that 15 years ago, Goldman Sachs expected to rule the 21st century; i.e., Brazil, Russia, India, China, and South Africa.