Since last week, the market began to speculate the Bank of Japan (BoJ) would withdraw the negative policy rate in the near future. The dollar-yen exchange rate fell by a few hundred points. However, BoJ has been very hesitant to withdraw policy accommodation.

Previously, the adjustment of yield curve control (YCC) was done so cautiously that only the cap of 10-year yield was raised to 1 percent, but the target remained at zero percent. Even in this round, the policy rate is moved to zero percent or slightly above, and the policy stance cannot be said to be tightening.

No doubt the lost decades were over, or now shifted to China. However huge the bubble by the end-1980s and however big the crash aftermath, two decades or five or six normal economic cycles should be enough to clean up most if not all of the problems. Although there should be no more debt deflation by now, whether there is strong inflation pressure is also doubtful. Japan is still experiencing a population decline that is getting even more serious, and tech advancement is yet another deflation generator.

This is evidenced from the past few years, where most Western countries suffered from high single-digit to double-digit inflation while Japan’s peaked at only 4 percent (by end-2022). This natural experiment due to COVID-19 suggests the high inflation episode is likely due to common shock rather than anything specific, but slight differences in inflation level could be a local issue rather than global. As such high episode fades out, Japan’s inflation is prone more to local factors than global. While Western countries have 3-4 percent persistent inflation, Japan’s inflation is at an ideal 2 percent.

In this sense, there is no need for BoJ to change its policy; in fact, their incentive to do so has been quite low. Another reason why they are reluctant to do so is the potential economic weakness ahead: Japan is having consecutive quarter-over-quarter GDP contraction.

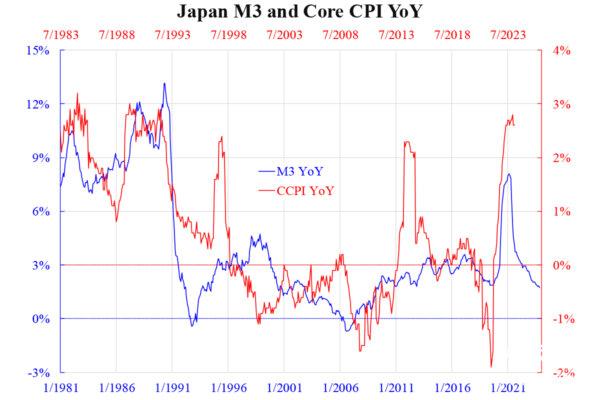

The accompanying chart shows the relationship between broad money (M3) and core CPI (CCPI), both expressed in year-over-year growth rate. Broad money is multiplied from narrow via the repeated lending and depositing process. Thus, its fast growth means lending improves.

Data confirm this clearly: Japan’s bank lending YoY growth between mid-2020 and mid-2021 shot up to over 6 percent compared to the previous trend of 2-3 percent. This drove up the M3 growth and hence inflation. Observation suggests inflation lags M3 growth by about two to three years.

Nevertheless, since then, the unexceptional high lending growth cannot be sustained. Now, it has returned to the near-normal level of 3 percent, albeit slightly higher than the previous 2-3 percent. This means inflation will follow suit.

Although core inflation is not always on track following the M3 growth path strictly on the chart, the direction is, by and large, correct. Accordingly, inflation is predicted to go down under this model. Policy tightening from now on would intensify the potential disinflation ahead. This explains why BoJ has been so reluctant to act despite being under huge market pressure.