Commentary

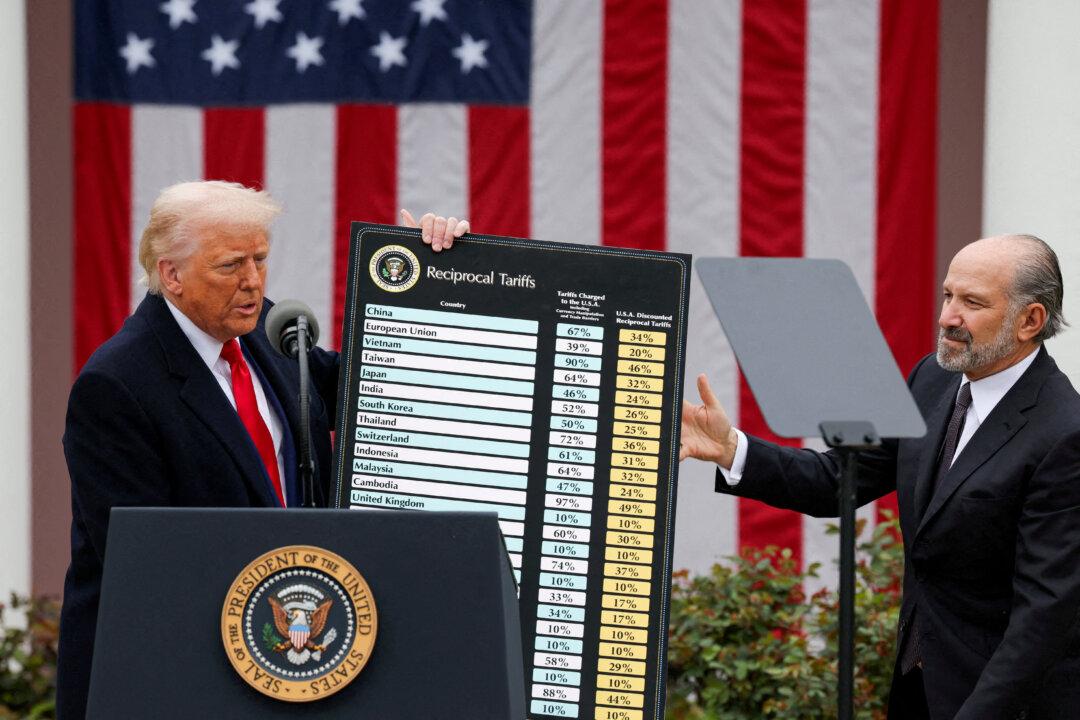

Since the Trump administration first levied tariffs on China, the open question has been how the tariffs will change international trade patterns.

Since the Trump administration first levied tariffs on China, the open question has been how the tariffs will change international trade patterns.