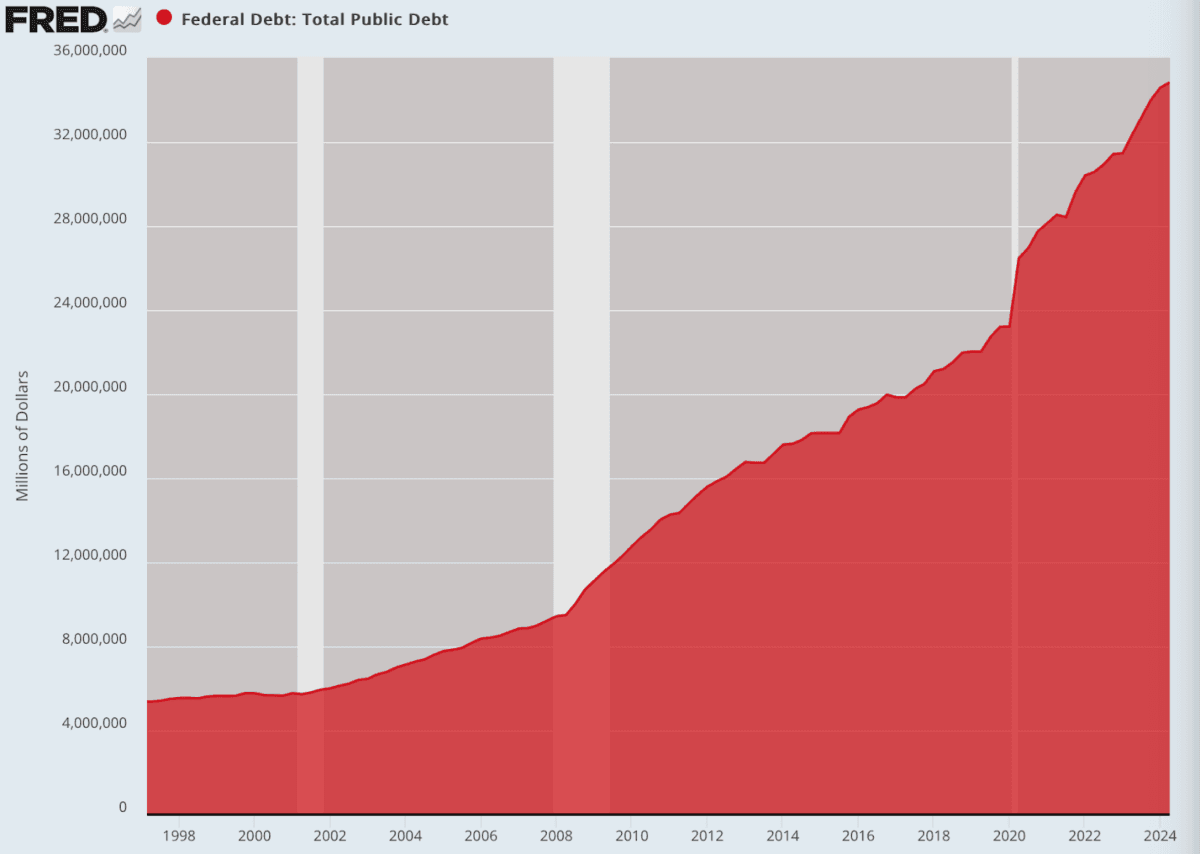

The national debt just hit $36 trillion, owing to a wild spending binge in the past year to create the impression of a booming economy. It did not work, but now we are left with an enormous fiscal mess that is not easily fixed without some real pain.

Part of the problem traces to a complicated issue about which no one outside the bond industry really cares. Treasury Secretary Janet Yellen and Fed Chair Jerome Powell have spent the past year carefully adjusting the Fed’s bond portfolio to hold short-term securities over the long term. The purpose was to lower the servicing costs to the U.S. Treasury, but that also means more frequent rollover periods.

This presents the Trump administration with a huge problem. The slightest issue to appear in bond markets could mean a real storm for fiscal policy starting in the first quarter. The Fed will have lost all flexibility to deal with it without making the existing inflation problem much worse.

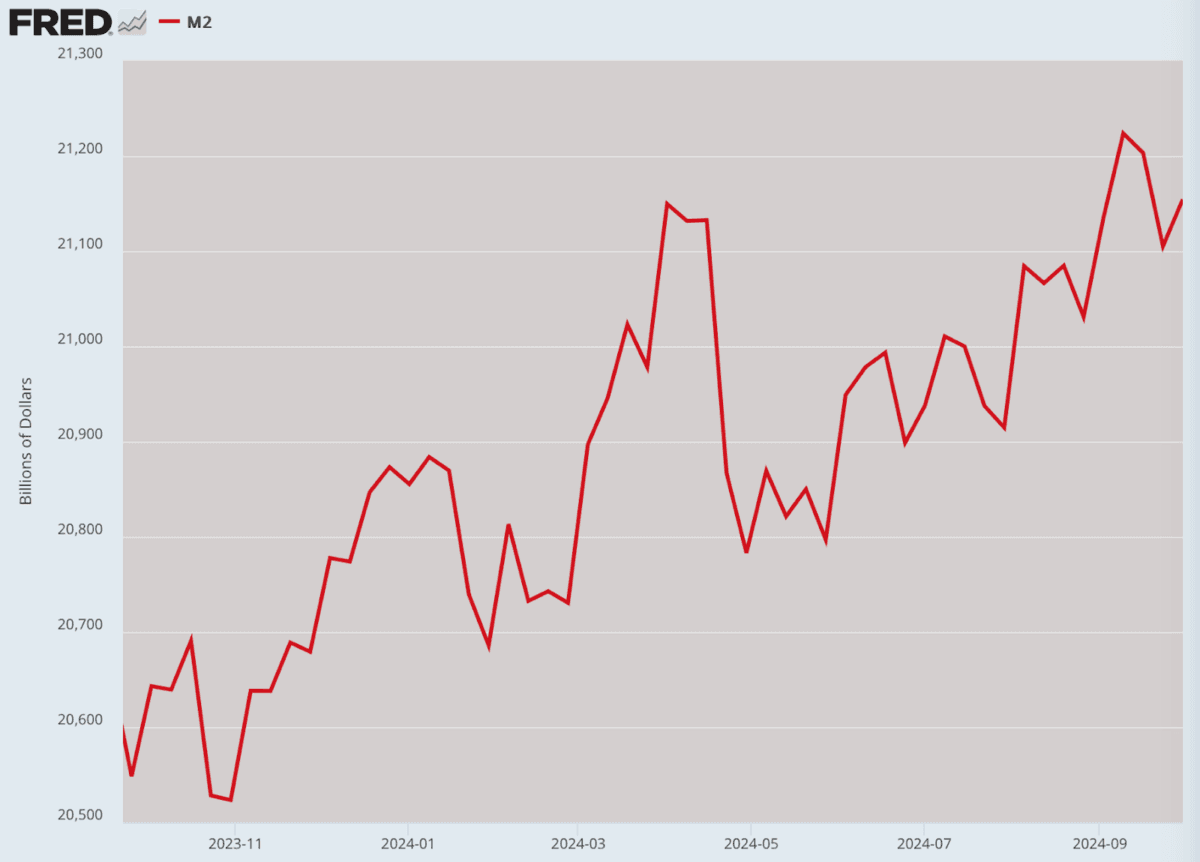

A look at M2 money aggregates doesn’t provide comfort either. We are up $1 trillion in money stock over the past year in a period of rising velocity.

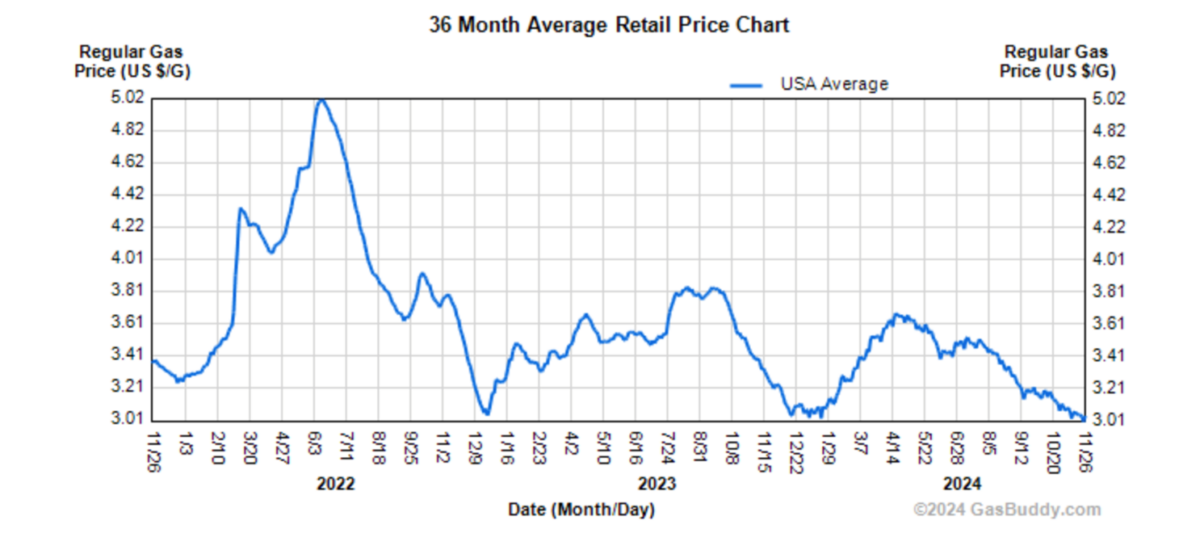

All that said, consider how oil and gas figure into this. Gas prices are falling rather dramatically, owing to a substantial change over 18 months from the Biden administration to push for more drilling and refining to bring down the price of gas in advance of the election. I’ve seen gas prices as low as $2.30 in Texas, and they seem to be trending downward.

On the campaign trail, it was common for Trump to claim that the whole inflation problem traces to the Biden administration’s emphasis on green energy and closing of pipelines, bringing about a cost-push effect for general prices. It’s not an implausible theory on its face, but it neglects a more obvious explanation in the money supply itself, which is up by $6.1 trillion over four years and rising.

There is no denying it at this point: “Drill baby drill” will be great for oil and gas prices, but it simply will not fix the problem of accelerating inflation. There is even an opposite danger here, that more production will reduce the price so much that the incentive to produce is reduced because of lower profitability. It’s the old problem of supply and demand, and its interaction with the price: Less is produced at a lower price than at a higher price.

In theory, such efforts hurt Iran, but they also reduce margins for U.S. producers.

That such complications are too much for the campaign trail is understandable. But it is a point that the Trump administration will have to deal with right away. Drilling alone will not solve all problems, even if it represents a welcome corrective to the “green energy” emphasis of the last administration.

Regardless of oil and gas, inflation will be made worse by the astonishing increases in government spending, which has produced a T-bill tsunami that the Fed is called upon to sponge up. That results in more inflation, the very thing that Trump has sworn to stamp out.

There can be no business as usual. The team called the Department of Government Efficiency must get to work and act immediately to address the massive spending problem, together with emergency-level regulatory cuts and agency elimination. That won’t solve the whole problem but it will at least inspire some confidence that it is fixable with dramatic action.

If nothing happens, the Trump administration will face a huge problem in the midterms. Having blamed Biden for the whole of inflation, rather inaccurately, it is now called upon to fix the whole of the problem immediately. That can only happen by stopping the spending and printing flood and creating an environment favorable to wealth creation.

How in the world can DOGE cut $2 trillion from the federal budget? The New York Times, Vox, and even The Wall Street Journal say it is impossible. A flurry of articles have all made this same claim. There are too many non-negotiables such as interest on the debt, Social Security, Medicare, and transfer payments. Cutting government salaries through attrition is a great idea, but it only gets you maybe 25 percent to 50 percent of the way there.

We are rightly skeptical of the myriad of mainstream media articles throwing cold water on the idea of spending and regulatory cuts. Obviously they do not want them because there is a strange and symbiotic relationship between the well-financed permanent government and the media, one of which we are more aware than ever.

One way to oppose a change is simply to announce that such a change is not possible. That might demoralize the advocates to stop trying.

But Elon Musk and Vivek Ramaswamy are not so easily cowed. They have both run huge companies and have enormous business experience. They are temperamentally allergic to waste and abuse. Leaking revenue and inefficiency offends them at every level. No matter how bad they think it is at the federal government, they will undoubtedly discover things neither believed possible.

Their determination to succeed at this is boundless. Maybe it cannot be done, but if anyone can do it, they can.

The financial markets, meanwhile, are obviously exuberant about the possibility of dramatic change. The Trump cabinet picks in the Treasury and elsewhere have buoyed the markets. Just getting an enterprise-friendly regime in charge in a couple of months has unleashed pent-up optimism.

That said, optimism cannot overcome accounting realities, and there is no question that the Trump administration will immediately have to deal with fiscal and monetary wreckage else risk the whole of the presidency. Trump knows this but has chosen to outsource the job to DOGE. This seems like a wise move.

A hidden reason for the optimism concerns the feeling that big tax cuts are coming. Perhaps it seems irresponsible to be talking about tax cuts when the debt is exploding and the budget is such a mess. That said, the right kind of aggressive spending cuts—approved by a Congress that should be fearful of defying an epically popular president—could make deep tax cuts fiscally possible and mitigate against the price hikes that will follow from aggressive tariff strategies.

These problems are not insurmountable, but they must be confronted—and right away.