For many investors who started their investing journey following the financial crisis of 2008–09, forward returns will be disappointing compared to the last decade. But it won’t be solely due to high valuations.

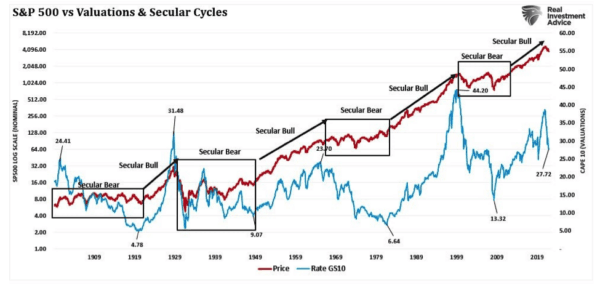

“Three items drive secular bull markets: 1) valuation expansion, 2) earnings growth, and 3) falling interest rates. The most prominent driver of secular returns are periods of valuation expansion and contractions.”

“The chart above shows the history of secular market periods going back to 1871 using data from Dr. Robert Shiller. You will notice that secular bull markets begin with CAPE [cyclically adjusted price-to-earnings ratio] valuations around 10 times earnings or even less. Secular bear markets tend to start with valuations of 23–25 times earnings or greater. (Over the long term, valuations do matter.) Most notably, secular BEAR market periods are defined by near-zero returns during the valuation contraction process.”

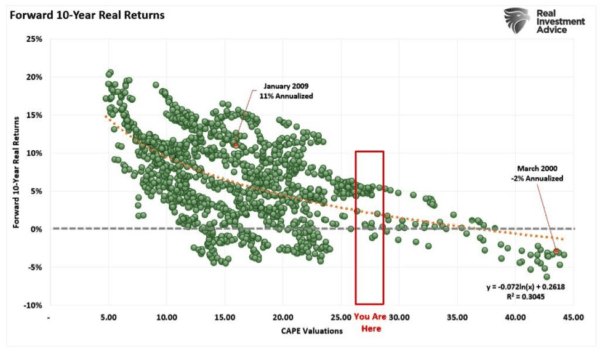

As we know, a decent correlation exists between future returns and current valuations.

As we have often stated, this does not mean that every year over the next decade will foster low returns. It only suggests that the total return will be low over the entire decade. History shows that such is the case.

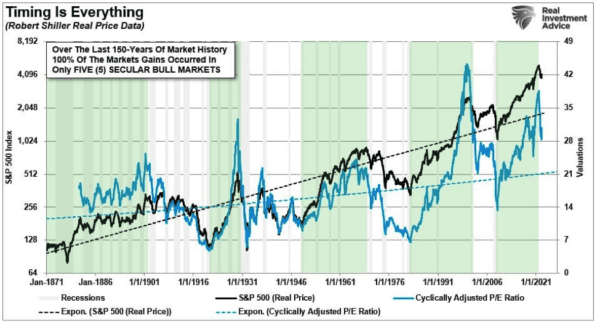

“Notably, as an investor, only five periods are secular bull markets (where prices are increasing) over the last 150 years. Those five periods account for 100 percent of all the index gains. In other words, the outcome was disappointing if you invested on a buy-and-hold basis during any other period.”

The Monetary Illusion of Growth

How often have you seen the following chart presented by an advisor suggesting that if you had invested 120 years ago, you would have obtained a 10 percent annualized return?

It is a true statement that, over the very long term, stocks have returned roughly 6 percent from capital appreciation and 4 percent from dividends on a nominal basis. However, since inflation has averaged approximately 2.3 percent over the same period, real returns averaged roughly 8 percent annually.

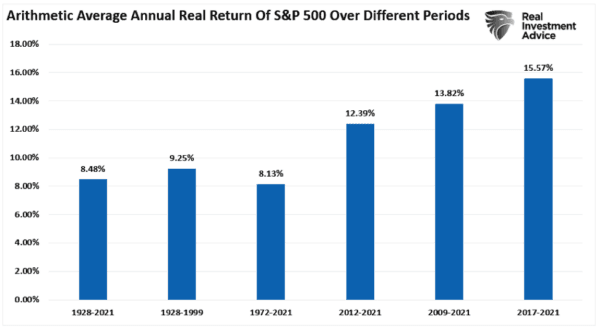

The chart below shows the average annual inflation-adjusted total returns (dividends included) since 1928. I used the total return data from Aswath Damodaran, a Stern School of Business professor at New York University. The chart shows that from 1928 to 2021, the market returned 8.48 percent after inflation. However, notice that after the financial crisis in 2008-09, returns jumped by an average of four percentage points for various periods.

After more than a decade, many investors have become complacent in expecting elevated rates of return from the financial markets. During that period, investors developed many rationalizations to justify overpaying for assets.

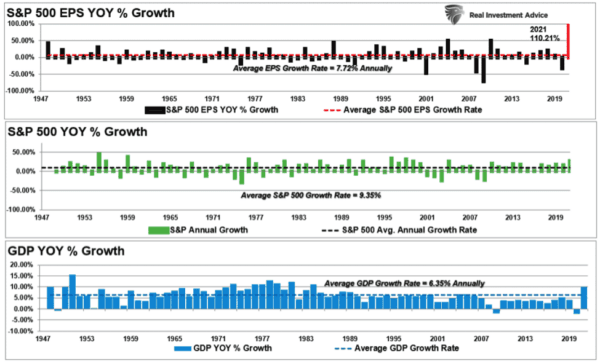

However, the problem is that replicating those returns becomes highly improbable unless the Federal Reserve and the federal government commit to ongoing fiscal and monetary interventions. The chart below of annualized growth of stocks, GDP, and earnings show the outsized anomaly of 2021.

Since 1947, earnings per share have grown at 7.72 percent, while the economy has expanded by 6.35 percent annually. That close relationship in growth rates is logical, given the significant role that consumer spending has in the GDP equation.

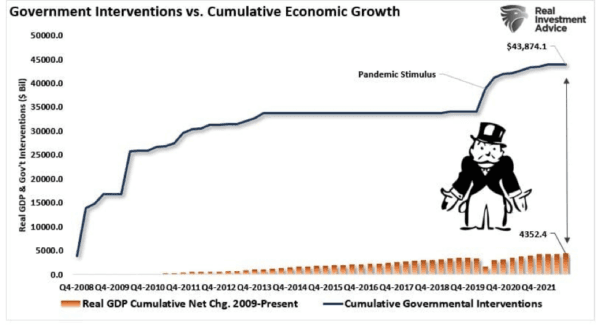

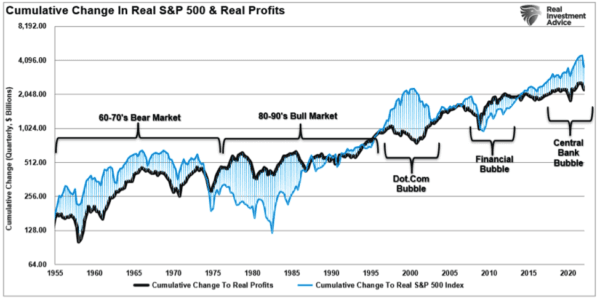

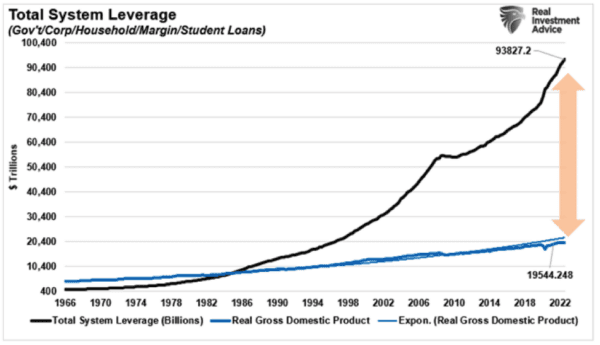

The market disconnect from underlying economic activity over the last decade was due almost solely to successive monetary interventions, leading investors to believe “this time is different.” The chart below shows the cumulative total of those interventions that provided the illusion of organic economic growth.

A Return to Normal

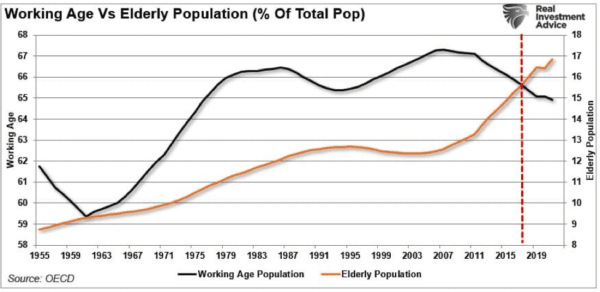

Over the last decade, massive monetary interventions distorted financial markets from their respective underlying economic linkages. As noted above, the deviation from long-term growth trends is unsustainable, particularly when factoring in demographic trends.Over the next decade, the elderly population will begin systematically withdrawing assets from the market for retirement. Given the rise in individuals approaching retirement against a declining working-age population, the problems for pension and welfare systems become more apparent.

Nonetheless, economic growth will run below previous trends between an aging demographic of accumulators becoming net distributors of assets and less monetary support in the future.

Therefore, returns must revert to historical norms. Such will result from profit margins and earnings returning to levels that align with actual economic activity.

Of course, one must also consider the drag on future returns from the excessive debt accumulated since the financial crisis.

That debt’s sustainability depends on low-interest rates, which can only exist in a low-growth, low-inflation environment. Naturally, a low-inflation and slow-growth economy do not support excess return rates.

It is hard to fathom how forward return rates will not be disappointing compared to the last decade. However, those excess returns were the result of a monetary illusion. The consequence of dispelling that illusion will be challenging for investors.

But then again, getting normal returns may be “feel” very disappointing to many.