China enthusiasts and supporters of the Beijing Consensus have mainly cited two elements as a proof of China’s invincibility.

The first is rapid GDP growth, mostly higher than 10 percent per year over the last two decades.

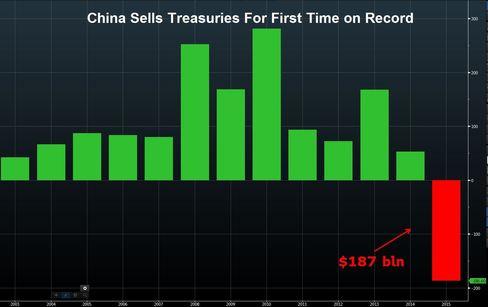

The second was an enormous stash $4 trillion in foreign exchange reserves. The emphasis here is on “was” because this stash since melted to $3.3 trillion at the end of 2015, the first annual decline on record and there is no end in sight.

Bloomberg