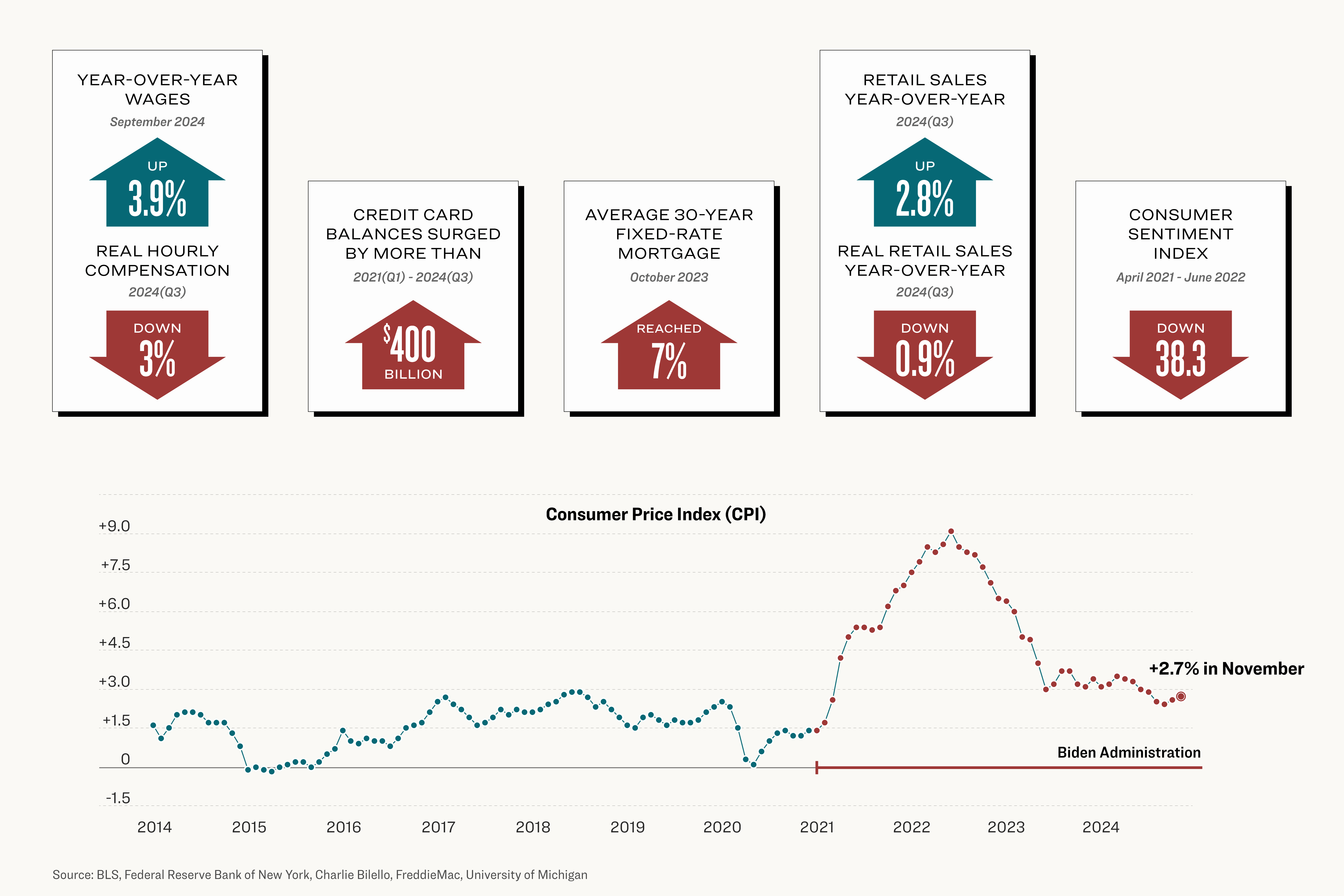

Trump to Inherit Years of Steep Inflation: 4 Things to Know

The incoming administration is faced with consumers who are struggling with high debt, high interest rates, and wages that haven’t kept up with inflation.

Inflation was the chief issue for millions of Americans going into the 2024 election.

When President Donald Trump left office in January 2021, the annual inflation rate was 1.4 percent. When he returns to the White House next month, the consumer price index (CPI) will be close to 3 percent.