The debt situation in the United States is looking increasingly precarious, and the country is on the brink of a fiscal crisis unless it takes steps to reduce its federal budget deficit and manage debt growth.

This is a warning from experts, including the International Monetary Fund (IMF), which said in a report last week that the astronomical increase in the U.S. national debt poses significant risks to the global economy, which also has the potential to further exacerbate high inflation.

In an unusually forthright criticism of U.S. policymakers, the global financial agency added that an unsustainable fiscal policy was partly responsible for the country’s recent strong performance among advanced economies.

In the latest World Economic Outlook, which is published twice a year, the IMF issued a warning on April 16. “The exceptional recent performance of the United States is certainly impressive and a major driver of global growth, but it reflects strong demand factors as well, including a fiscal stance that is out of line with long-term fiscal sustainability,” the IMF wrote.

This creates short-term risks to the disinflation process as well as longer-term fiscal and financial stability concerns for the global economy since it increases global finance costs, the IMF stated, adding, “Something will have to give.”

Ever since October of last year, various organizations, such as think tanks, the Government Accountability Office (a government watchdog), and the Congressional Budget Office (Congress’s budget and economic information source), have been warning about the loose fiscal policy in the United States.

According to them, this policy is causing global interest rates and the dollar to rise, as well as increasing funding costs in other parts of the world, which in turn worsens existing fragilities and risks.

Federal deficit spending has been driven in recent years by COVID 19-related stimulus, aggressive investments in infrastructure and clean energy, and exploding interest costs. The Congressional Budget Office, for example, projects that public debt will rise to $45.7 trillion, or 114 percent of GDP, by 2033, from 97 percent at the end of 2023.

Despite the growing concerns, Treasury Secretary Janet Yellen has consistently sought to downplay them, emphasizing that the cost to service debt as a percentage of GDP, adjusted for inflation, should be the measure of debt sustainability.

Autopilot Hazards

Yet “if current policies were left on autopilot, U.S. debt-to-GDP would near double over the next 30 years,” says Ryan Bourne, R. Evan Scharf Chair for the Public Understanding of Economics at Cato Institute.Mr. Bourne told The Epoch Times that the current debt level has surged to its highest point since World War II and is predicted to reach 106 percent of GDP, which would be the highest level of U.S. debt held by the public relative to the size of the economy ever.

Following the world war, the United States demilitarized, followed a policy of approximately balanced budgets for a quarter century, enjoyed rapid economic expansion, and had two periods of devastating inflation, all of which lowered the actual debt load.

Still, the United States continues to run massive deficits with an aging population weighing on growth, and the entitlements that will fuel the debt in the coming decades are inflation-protected.

Geopolitical Challenges

Experts fear that the rapidly mounting debt load could have several complications down the road.“The poor fiscal discipline of the U.S. could end up with an exponential explosion in government indebtedness,” Gary Dugan, CEO at The Global CIO Office and a foreign investor in the United States, told The Epoch Times.

Aside from stifling economic growth over time, high debt levels can also lead to higher interest rates, which in turn can dampen investment and consumption, ultimately affecting overall economic vitality.

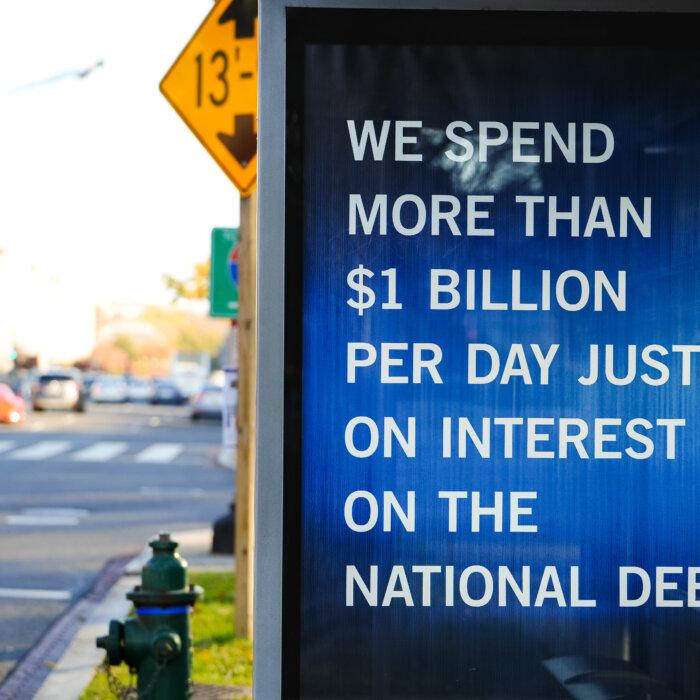

As the debt grows, so do the interest payments on it. These payments divert resources away from other essential government programs. In fact, the federal government currently spends as much on interest payments as it does on most safety net programs combined, suggest report. As interest costs rise, the government’s ability to invest in new priorities becomes limited.

“If investors lose confidence in the United States’s commitments to pay back its debt, bond yields will spike, leading to more borrowing and driving up yields further in a fiscal doom loop,” says Mr. Bourne.

This scenario could result in various forms of volatility in global asset prices. There might be a sudden rush to withdraw investments from dollar-denominated assets as well if investors anticipate the federal government pressuring the Federal Reserve to directly fund government expenditures.

“We expect this increasingly to weigh on the U.S. dollar with a bias to a weaker dollar over the medium term; [besides] do note that the U.S. small company index is at a 11-year low, showing that the economy is not universally strong,” Mr. Dugan said.

But according to Robert Swift, chief investment officer at Sydney-based Delft Partners, a significant portion of the U.S. debt is held by foreign investors. Consequently, a substantial share of national income flows abroad. This leaves the United States with fewer financial tools to manage conflicts with other countries when they have increased leverage over the American economy.

Path Forward

Nevertheless, the Cato Institute suggests that given the urgency of the situation, Congress should currently focus on crafting a comprehensive deficit reduction plan.“To get inflation back to 2 percent consistently requires the Federal Reserve to set a monetary stance consistent with getting a steady growth of total spending on final goods and services [nominal GDP] of about 3–4 percent per year,” said Mr. Bourne. “Right now, it’s around 5.7 percent, which shows that monetary policy was too expansive 18 months ago.”

Reducing the deficit would also require significant changes to entitlement programs and a thorough reassessment of the government’s role, with a focus on reducing spending, commented the Cato Institute.

If Congress is unable or unwilling to achieve this, it would be advisable to prioritize reducing everyday expenses before resorting to tax increases that could hinder economic growth.

Still, the IMF praised the economic growth of the United States, despite inflation and increasing debt.

According to the agency, the U.S. economy is projected to grow by 2.7 percent this year, which is a 0.6 percent increase from January’s projection. In addition, the United States added 2.7 million jobs last year.

The agency’s chief economist attributes the United States’s strong performance to robust productivity and employment growth, as well as strong demand in an overheated economy.

“This calls for a cautious and gradual approach to easing by the Federal Reserve,” the IMF report said.

Meanwhile, the Bureau of Economic Analysis reported on Friday that the Personal Consumption Expenditures (PCE) price index, which is the Federal Reserve’s preferred measure of inflation, increased more than anticipated in March. The headline PCE price index rose from 2.5 percent in February 2024 to 2.7 percent year over year in March, surpassing the predicted 2.6 percent rise.

While the inflation measure came in too high for a near-term rate reduction in March, but not as terrible as expected, ruling out a Fed rate cut this year, Mr. Swift said: “The era of very cheap money and crap stocks being floated on the market is over.”